Direct Answer: Not all dentists accept or understand Medicare Advantage dental benefits. Before booking, ask specifically whether they’re in-network with your plan and what’s actually covered.

If you’re enrolled in a Medicare Advantage plan and you live in Surprise or the surrounding West Valley, you’ve probably already discovered that dental benefits under these plans can be confusing. The coverage varies dramatically from one plan to the next — and a lot of dentists don’t fully understand how to work with them.

Many retirees in communities like Sun City Grand, Sun City, and The Grand come in every year asking the same questions: Does my plan cover this? Why did I get a bill after my cleaning? What’s the difference between what Medicare covers and what my Advantage plan covers? These are fair questions, and the answers aren’t always simple.

This article breaks down the parts that actually matter — what Medicare Advantage dental coverage typically looks like, what questions to ask your dentist’s office before you commit, and what to watch for when benefits reset each year.

What Medicare Advantage Dental Coverage Actually Covers

Original Medicare — Parts A and B — covers almost nothing dental. No routine cleanings, no fillings, no crowns. The only dental care traditional Medicare touches is something directly connected to a covered medical procedure, like jaw reconstruction after a hospital stay.

Medicare Advantage plans (Part C) are different. Many of them do include dental benefits, but those benefits are added by private insurers, not the federal government. That means coverage varies widely depending on which plan you chose during open enrollment.

Most basic Medicare Advantage dental plans cover:

- Two cleanings per year (sometimes one)

- Routine X-rays — usually bitewings once a year, full mouth every 3-5 years

- Oral exams — typically two per year

- Fluoride treatments for qualifying patients

More generous plans — sometimes called enhanced or comprehensive dental riders — also cover a portion of fillings, extractions, crowns, or dentures. But even those plans usually come with an annual maximum benefit, often in the range of $1,000 to $2,500 per year. Once you hit that ceiling, you’re paying out of pocket for the rest of the calendar year.

If you’re not sure what tier your plan includes, your insurance card should have a member services number. Call them and ask for your dental benefits summary in plain language before scheduling any restorative work.

Why Some Dentists Struggle With Medicare Advantage Plans

Medicare Advantage is not one insurance — it’s dozens of separate private plans, each with different fee schedules, prior authorization rules, and claim processes. A dentist who accepts Humana Medicare Advantage isn’t automatically in-network with Aetna Medicare Advantage or UnitedHealthcare Medicare Advantage.

This creates real problems for patients. You might assume your dentist takes your insurance because they said they take Medicare, only to find out at checkout that your specific plan wasn’t on file. That mismatch can mean you’re billed at out-of-network rates — or worse, you receive a surprise bill weeks after your appointment.

For patients with more complex dental needs, there’s another layer: some Medicare Advantage plans require prior authorization before the dentist can place a crown or perform an extraction. If your provider doesn’t know to request that authorization first, the claim can be denied even when the service would otherwise be covered.

A few things worth checking before any appointment:

- Ask the front desk to verify your specific plan by name and member ID, not just “Medicare”

- Ask whether your planned treatment requires prior authorization under your plan

- Ask for an estimated patient portion in writing before the appointment

- Confirm whether your plan pays the dentist directly or reimburses you after the fact

If the front desk team can’t answer those questions, that’s a signal worth paying attention to. Offices that work regularly with Medicare Advantage patients have these conversations every day — it shouldn’t feel like you’re asking something unusual.

For context, what to look for in a dentist after you retire covers many of these same considerations if you’re evaluating a new dental home.

Medicare Advantage Dental: Basic vs. Enhanced Plans at a Glance

Coverage between plan tiers varies significantly. Here’s a general comparison of what patients in the West Valley typically encounter.

| Service | Basic Plan Coverage | Enhanced Plan Coverage |

|---|---|---|

| Routine cleanings | 1-2 per year, covered 100% | 2 per year, covered 100% |

| Dental X-rays | Bitewings annually | Full mouth + bitewings covered |

| Fillings | Not covered or limited | 50-80% after deductible |

| Crowns | Not covered | 50% up to annual max |

| Dentures | Not covered | 50% with waiting period |

| Extractions | Emergency only, sometimes | Covered at 50-80% |

| Annual maximum benefit | $0-$500 | $1,000-$2,500 |

| Orthodontics / Implants | Not covered | Rarely covered; plan-specific |

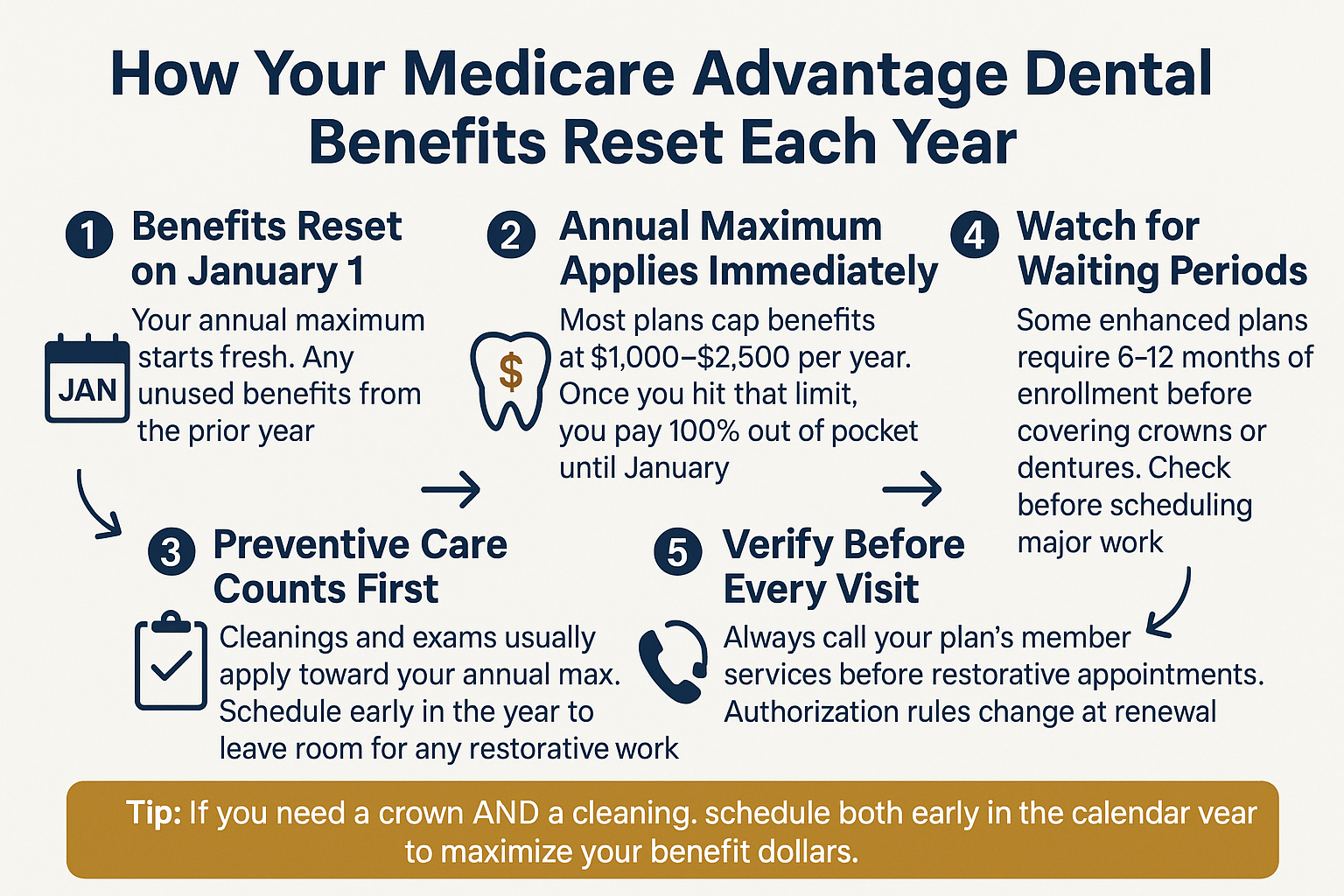

How Medicare Advantage Dental Benefits Work Year to Year

This infographic walks through how annual benefit cycles affect your dental care decisions — especially for patients with restorative needs.

When Benefits Reset: Timing Your Care to Stretch What You Have

One of the most practical things a dentist’s office can do for Medicare Advantage patients is help them understand the benefit year calendar and plan accordingly.

Most plans reset on January 1. That means if you’ve already used $1,800 of a $2,000 annual maximum by October, you have two realistic options: hold off on non-urgent work until January, or accept that you’ll be paying mostly out of pocket for anything done before year-end.

For retirees in Sun City Grand or Copper Canyon Ranch who might be dealing with older dental work that needs attention — worn crowns, failing old fillings, partial denture adjustments — this timing question comes up a lot. A dentist who understands your plan can help you sequence treatment across two calendar years to make your benefits go further.

For example, if you need two crowns, placing one in late December and one in early January means each crown draws from a separate year’s maximum. That’s a real difference, especially when a crown typically runs $1,200 to $1,800 in the Surprise area without insurance.

And if you’ve been putting off a cleaning because you weren’t sure if it was covered, that’s a situation worth revisiting. Skipping cleanings can lead to the kind of problems that end up costing far more down the road, regardless of what your plan covers.

The front desk team at any practice that regularly works with Medicare Advantage patients should be willing to review your remaining benefits before you commit to a treatment plan. If they can’t do that, find a practice that can.

What to Actually Ask Before You Book

Knowing the right questions can save you real money and real frustration. Before scheduling any dental appointment — especially for work beyond a cleaning — ask the office these specific questions:

- “Are you in-network with [plan name, not just Medicare Advantage in general]?” Get the plan name off your card and use it exactly.

- “Does my plan require prior authorization for this treatment?” Fillings usually don’t. Crowns and extractions often do.

- “Can you give me an estimated out-of-pocket cost before the appointment?” A good office will verify benefits and provide a written estimate.

- “Do you bill my plan directly, or do I need to submit a claim myself?” Most in-network providers bill directly, but some smaller offices still require patient-submitted claims.

- “How much of my annual maximum have I already used this year?” The office can pull this with your member ID if they’re experienced with your plan.

These aren’t difficult questions. An office that works with Medicare Advantage patients regularly will have answers ready. If the response is vague or they suggest calling the insurance company yourself for everything, that’s worth factoring into your decision.

For patients weighing whether to address a tooth that’s been bothering them for a while, this article on when a missing or broken tooth should be restored is a useful starting point before that insurance conversation even happens.

Frequently Asked Questions About Medicare Advantage and Dental Care

Does Medicare Advantage cover dental implants?

Rarely. Most standard Medicare Advantage plans do not cover dental implants. A small number of enhanced or supplemental dental riders do offer partial coverage — sometimes 50% up to the annual maximum — but this varies by insurer and plan tier. Always call member services and ask specifically about implant coverage, including whether a bone graft (which is often needed before implant placement) is a separate benefit category.

My plan says it covers ‘preventive dental care.’ What does that actually mean?

In insurance terms, preventive care typically means cleanings, routine exams, and X-rays. It does not include fillings, crowns, or extractions, which fall under ‘basic’ or ‘major’ service categories — and those often require a separate cost-share from you.

Can I use my Medicare Advantage dental benefits at any dentist?

Only if that dentist is in-network with your specific plan. If you see an out-of-network dentist, you’ll either pay full price or be reimbursed at a lower rate depending on your plan’s out-of-network policy. Always confirm network status before your first appointment — not just once, since networks can change at annual enrollment.

What happens if I need a crown and I’m close to my annual maximum?

If you’ve nearly hit your annual cap, you have a few options. You can wait until January 1 when benefits reset. You can ask whether your plan allows a predetermination of benefits — a formal review that tells you in advance exactly what they’ll pay. Or you can ask the dental office about an in-house payment plan for the remaining balance. A practice experienced with Medicare Advantage patients will walk you through the math before you decide.

Is Medicare Open Enrollment really the time to reconsider my dental coverage?

Yes. Medicare Advantage Open Enrollment runs from October 15 through December 7 each year. If your current plan’s dental coverage has been disappointing — low annual maximum, poor coverage for fillings or crowns, limited network — this is the window to switch to a plan with stronger dental benefits for the following year. Compare plans on Medicare.gov or call your State Health Insurance Assistance Program (SHIP) for free one-on-one help.

I’ve avoided the dentist for years. Will my Medicare Advantage plan cover the catch-up care I need?

That depends on your plan tier and what’s needed. Cleanings and exams are almost always covered at least partially. But if you need multiple fillings, crowns, or extractions after a long gap, your annual maximum may not cover everything in a single year. A good dental office will help you prioritize the most urgent care first, sequence the rest across benefit years, and work with you on financing for anything that falls outside your coverage.

Have Questions About Your Medicare Advantage Coverage?

Our team at West Bell Dental Care works with Medicare Advantage patients every day — verifying benefits, coordinating prior authorizations, and helping patients in Sun City Grand, Sun City, and across Surprise plan their care around their annual maximums. If you’re not sure what your plan covers or you’d like to talk through your options before scheduling, you can reach us at 480-795-2420 or visit westbelldentalcare.com. We offer Saturday appointments for patients who need a little more flexibility.