Welcome to your complete guide to understanding dental insurance. Let's be honest, trying to make sense of dental benefits can feel like putting together a puzzle with half the pieces missing. It doesn't have to be that complicated. This guide is your roadmap, written specifically for our neighbors in Surprise, Sun City, and Peoria who want to feel confident about their oral healthcare choices.

Your Guide to Navigating Dental Insurance

We're going to break down those confusing insurance policies into simple, easy-to-digest concepts. Think of us as your friendly translator for all things deductibles, copays, and plan types. Our main goal is to give you the tools you need to pick the right plan for your family and really get the most value out of your coverage.

By starting with the basics and building up from there, we'll help you see how you can get top-notch care at West Bell Dental Care without the financial stress or confusion.

Making Sense of Your Coverage

At its core, dental insurance is a health benefit designed to help pay for a portion of your dental care costs. But here’s a key difference from your regular medical insurance: dental plans are built around prevention. This is why you’ll often see routine services like cleanings and check-ups covered at a high percentage—they want to help you stay healthy from the start.

This focus on prevention is becoming more crucial than ever. According to the CDC, nearly half of adults over 30 show signs of gum disease. Regular, covered dental visits are the best way to catch and manage issues like this early on.

Your Partner in Oral Health

Truly understanding your plan is the first step toward a healthier smile. It's simple: when you know what’s covered, you’re far more likely to get the preventive care that keeps your teeth and gums in great shape. Being proactive is the best way to avoid bigger, more expensive procedures down the road.

Here at West Bell Dental Care, we see ourselves as your partners in this journey. Our team is dedicated to helping patients in Surprise, AZ, and our surrounding communities like Sun City West and El Mirage make the most of their benefits every single day. Whether you're here for a routine check-up or a more involved treatment, our approach to general dentistry in Surprise, AZ always focuses on your long-term wellness. We're here to help you navigate your plan with total confidence.

Decoding Your Dental Insurance Policy

Opening your dental insurance policy can feel like trying to read a foreign language. All that jargon can be intimidating, but getting a handle on these key terms is the first step toward actually using your benefits wisely. Think of this section as your personal translator for making sense of it all.

We'll walk through the most common terms you'll run into, like premium, deductible, copayment, and annual maximum. By the time you're done, you’ll be able to look at your benefits summary with confidence, knowing exactly what your plan covers and what you're responsible for paying.

Your Monthly Membership Fee: The Premium

Think of your dental insurance premium as a monthly subscription fee, like Netflix or the gym. It's the fixed amount you pay every month to keep your plan active, whether you see the dentist or not. This payment is the foundation of your plan's cost.

To really understand your policy, it's helpful to know the basics, including how health insurance premiums are defined and calculated. Paying this premium is what keeps your access to dental care benefits open and available for when you need them.

Paying Your Entry Fee: The Deductible

Before your insurance company starts chipping in for most services, you’ll likely need to meet your deductible. You can think of this as a kind of entry fee for your benefits—a set amount of money you must pay out-of-pocket for certain covered services each year.

For instance, if your plan has a $50 deductible, you pay the first $50 of your dental treatment costs yourself. Only after you've paid that amount does your insurance start to share the costs with you.

Key Takeaway: Here's some good news. Preventive services like cleanings and check-ups often bypass the deductible entirely. It's your insurance plan’s way of encouraging you to stay on top of routine care!

Splitting the Bill: Coinsurance and Copayments

Once you've met your deductible, you’ll start sharing costs with your insurance provider. This usually happens in one of two ways:

- Coinsurance: This is a percentage of the cost you pay for a covered service. If your plan has 80% coinsurance for fillings, the insurance pays 80% of the bill, and you cover the remaining 20%.

- Copayment (or Copay): This is a simple, flat fee you pay for a specific service. For example, your plan might require a $25 copay for every office visit, no matter what treatment you receive that day.

Getting a grip on these cost-sharing elements is key to predicting what you'll owe for any given procedure.

The Plan’s Spending Limit: The Annual Maximum

The annual maximum is the absolute most your dental insurance plan will pay for your care within a single plan year. Once you hit this limit, you are responsible for 100% of any additional costs until your plan resets, usually at the start of the next year.

Knowing your annual maximum is critical, especially when you're planning for major dental work. Our team at West Bell Dental Care helps patients in Surprise, AZ, strategize their treatments to make the most of their benefits before the year ends.

For anyone worried about hitting this cap, exploring options like our in-house savings plan can provide real peace of mind. You can learn more about the benefits of our dental membership club—it’s a great alternative or supplement to traditional insurance.

Finally, understanding the difference between in-network and out-of-network is huge. As an in-network provider, West Bell Dental Care has already negotiated discounted rates with many insurance companies. Choosing an in-network dentist in Surprise, AZ, is one of the simplest ways to significantly lower your dental care costs right from the start.

Comparing the Most Common Dental Plans

Not all dental insurance plans are the same, and picking the right one can feel like a big decision for your family's health and finances. For our patients here in Surprise and Sun City West, understanding dental insurance is all about knowing the real-world differences between the most common types of plans. Let's break down the main options so you can see which one truly fits your life.

Think of it like choosing a cell phone plan—some have a higher monthly fee but give you more freedom, while others are cheaper but come with more restrictions. The "best" one really just depends on what you need.

Dental Plan Showdown: PPO vs. DHMO vs. Indemnity

To make things easier, let's put the three big players side-by-side. This table gives you a quick snapshot of how PPO, DHMO, and Indemnity plans stack up against each other when it comes to the things that matter most: cost, choice, and how they work.

| Feature | PPO (Preferred Provider Organization) | DHMO (Dental Health Maintenance Organization) | Indemnity (Fee-for-Service) |

|---|---|---|---|

| Provider Choice | High. Visit any dentist, but save more with in-network providers. | Low. Must use a dentist from the plan's exclusive network. | Highest. Visit any licensed dentist you want, with no networks. |

| Cost (Premiums) | Moderate to high monthly premiums. | Typically the lowest monthly premiums. | Often the highest monthly premiums. |

| Out-of-Pocket Costs | You pay deductibles and coinsurance. Costs are lower in-network. | Low or no copays for routine care. No deductibles or maximums. | You pay a deductible and a percentage of the costs (coinsurance). |

| Referrals to Specialists | Usually not required. | A referral from your primary care dentist is almost always required. | Not required. You can see any specialist directly. |

| Out-of-Network Care | Covered, but at a lower percentage, meaning you pay more. | Generally not covered, except for some emergencies. | Fully covered, as there are no networks to begin with. |

| Paperwork | Minimal. The dentist's office (like ours!) usually files claims for you. | Very little. No claims to file. | You may need to pay upfront and file your own claim for reimbursement. |

Seeing them laid out like this really highlights the trade-offs. DHMOs are budget-friendly but restrictive, Indemnity plans offer total freedom but at a higher price, and PPOs strike a balance right in the middle. Now, let's dive a little deeper into each one.

PPO (Preferred Provider Organization)

PPO plans are probably the most popular choice, and for good reason. They offer a great mix of flexibility and savings. The insurance company creates a "preferred" network of dentists who've agreed to provide services at a discounted rate.

Here's the deal with a PPO:

- Freedom to Choose: You can see any dentist you like, whether they’re in that network or not.

- Save Money In-Network: You'll pay the least out-of-pocket when you visit an in-network dentist, like West Bell Dental Care, because the insurance covers more of the bill.

- Coverage Outside the Network: If you decide to see a dentist who isn't in the network, your plan will still help pay, but your share of the cost will be higher.

For families in Surprise, AZ, who want the flexibility to pick their own doctor without being locked in, a PPO is often the perfect fit.

DHMO (Dental Health Maintenance Organization)

You can think of a DHMO as being more like a club membership. These plans usually have the lowest monthly premiums, making them a very attractive option if budget is your top priority. That lower cost, however, comes with less choice.

The key features of a DHMO are:

- Primary Care Dentist: You have to select a primary dentist from the plan's network, and that dentist manages all your care.

- Referrals are a Must: Need to see a specialist like an orthodontist or oral surgeon? You'll need to get a referral from your primary dentist first.

- No Out-of-Network Benefits: With very few exceptions for emergencies, DHMO plans simply won't cover any services from a dentist outside their network.

If you don't already have a dentist you love and your main goal is to keep monthly expenses down, a DHMO can be a smart, cost-effective choice.

Indemnity (Fee-for-Service) Plans

Indemnity plans, sometimes called traditional or fee-for-service plans, offer the most freedom, period. There's no network to worry about—you can go to literally any licensed dentist you choose.

With an indemnity plan, the process is a bit different. You usually pay the dentist for the full cost of your treatment first. Then, you submit a claim form to the insurance company, and they send you a check to reimburse you for a percentage of the cost. The biggest trade-off for all this freedom? Indemnity plans typically have the highest monthly premiums.

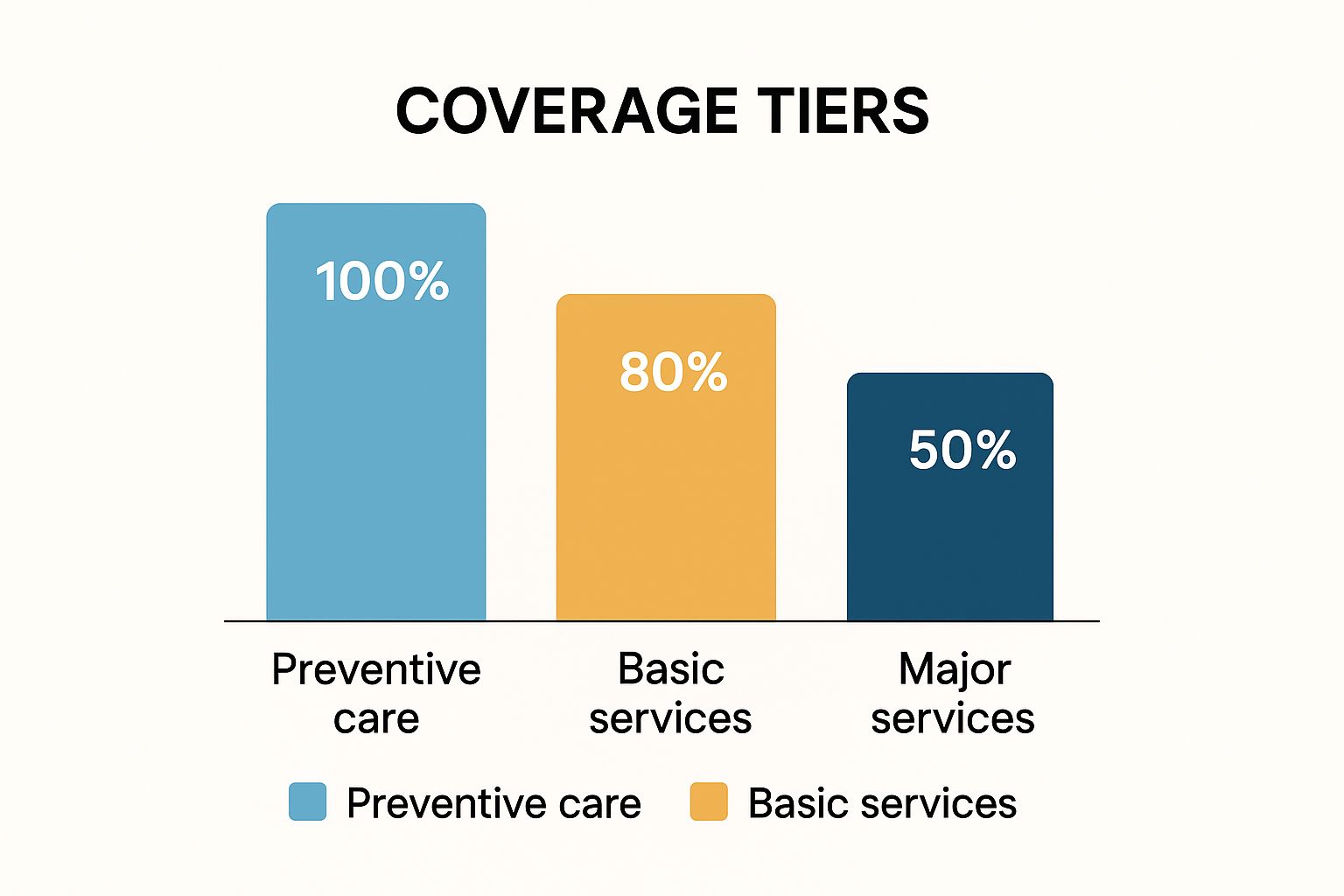

The image below shows the common 100-80-50 coverage structure that many PPO and indemnity plans use. It’s a great way to understand how your insurance pays for different types of treatment.

As you can see, this structure heavily favors preventive care like cleanings and checkups. Keeping up with those appointments isn't just good for your health—it’s the smartest way to use your dental benefits.

What About Dental Discount Programs?

It's also important to bring up dental discount programs because they're often mistaken for insurance, but they are not the same thing. A discount program is a membership club. You pay an annual fee, and in return, you get access to lower, pre-negotiated rates from a group of dentists who participate in the program.

Important Distinction: With a discount plan, there are no deductibles, no waiting periods, and no annual maximums. You don't file claims. You just pay the dentist the discounted price at the time of your appointment. It's simple and can save you money, but it doesn't provide the same financial safety net for major, expensive procedures that true insurance does.

What Your Dental Insurance Actually Covers

It’s one of the first questions we hear from our patients here in Surprise, AZ: "What will my insurance really pay for?" It’s the heart of the matter when it comes to understanding dental insurance, and the answer isn't always a simple one. Let’s break down how your coverage is typically structured so you can plan for your care without any financial curveballs.

Most dental plans don’t treat all procedures equally. Instead, they organize treatments into different levels of coverage. Think of it as a tiered system where your plan pays more for services that keep you healthy and a little less for more complex repairs.

The 100-80-50 Coverage Rule Explained

A lot of dental PPO and indemnity plans use a common structure called the 100-80-50 rule. It’s a pretty straightforward formula that outlines the percentage your insurance provider will likely pay for different types of dental work after you’ve met your deductible.

-

100% Coverage for Preventive Care: This is all about stopping problems before they start. Your plan wants to encourage you to stay on top of your oral health, so it often covers these appointments completely. This includes routine cleanings, regular exams, and annual X-rays.

-

80% Coverage for Basic Procedures: This category is for routine restorative treatments that are fairly simple. If you get a cavity or need a minor fix, your insurance will usually pick up a big chunk of the bill. Think fillings and simple tooth extractions.

-

50% Coverage for Major Procedures: This last tier is for the more complex and expensive restorative work. These are the treatments needed to address significant dental issues. Services here often include things like dental crowns, bridges, and root canals.

This tiered system actually reveals a major trend in healthcare. Preventive care holds the biggest market share in the growing dental insurance industry, showing that people are focused on maintaining their health before issues get worse.

Understanding Exclusions and Limitations

While the 100-80-50 rule is a great starting point, it's just as critical to know what your plan won’t cover. Every policy has specific exclusions and limitations to manage costs, and knowing what they are can save you from a surprise bill.

Here are some common limitations to look for:

- Waiting Periods: Many plans make you wait a certain amount of time (often six to twelve months) before they’ll cover major procedures like a crown or bridge.

- Cosmetic Exclusions: Treatments done only for looks, like teeth whitening or porcelain veneers, are almost never covered by standard dental insurance.

- Missing Tooth Clause: Some policies have a "missing tooth clause." This means they won't pay to replace a tooth that you lost before you signed up for the plan.

How Specific Treatments Are Handled

Getting a realistic idea of what you might pay for bigger treatments is key. Here’s a quick look at how insurance typically sees a few common procedures for our patients in Surprise and Sun City.

Dental Implants: This is a big one. Implants are often classified as a major procedure, and sometimes even a cosmetic one, so coverage can vary wildly. Some plans will cover a portion, while others won't cover them at all. Because they are such a permanent and effective way to replace a tooth, it's vital to check your policy's specific language. We have more information on the benefits of dental implants in Surprise and can help you figure out your coverage.

Braces and Orthodontics: Orthodontic coverage is usually not part of a standard dental plan. It’s often sold as a separate add-on or rider and typically has a lifetime maximum benefit for each person, which is separate from your plan's regular annual maximum.

Emergency Care: If you have a dental emergency in Peoria or a nearby town, your plan will usually cover the treatment based on what you need. For example, a broken tooth might need a filling (a basic service) or a crown (a major service), and your coverage will follow that category.

Your Financial Advocates: At West Bell Dental Care, our team is on your side. We’ll verify your benefits, give you clear cost estimates before any treatment begins, and handle the claims process for you. Our goal is simple: to make your dental care transparent and free of stress.

Choosing the Right Dental Plan for Your Family

Picking the right dental plan is easily one of the most important healthcare choices you'll make for your family. It's all about striking that perfect balance between what you can afford and the specific care your family actually needs. We put this guide together to help our patients in Surprise and El Mirage feel confident in that decision.

We'll walk you through the key questions you should be asking. What kind of dental work do you see on the horizon this year? Do you have a teenager who might need braces? Is having the freedom to see any dentist a big deal for you, or would you rather have a smaller network to keep costs down? Getting these answers straight first makes comparing plans a whole lot easier.

Assessing Your Family’s Dental Needs

Before you even glance at a single plan, just take a minute to think about your family's oral health history and what's coming up. A family with young kids has totally different needs than a retired couple. Having a clear picture of what you'll likely need is your best weapon for finding a plan that doesn't waste your money.

Start with these practical questions:

- Routine Care: Is your main goal just to cover regular check-ups and cleanings? If that's the case, a more basic, lower-premium plan might be a perfect fit.

- Existing Issues: Is anyone in the family dealing with ongoing problems, like a tendency for cavities or gum disease? If so, you'll want a plan with solid coverage for those basic and major services.

- Orthodontics: Are braces for your teenager a real possibility soon? A lot of standard plans won't touch orthodontia, so you might need to hunt for a plan with a special orthodontic add-on or benefit.

- Major Work: Are you or your spouse thinking about bigger procedures like crowns, bridges, or even dental implants in the near future? In that situation, paying a bit more in premiums for a plan with a lower deductible and a higher annual maximum could literally save you thousands of dollars.

Balancing Premiums with Out-of-Pocket Costs

One of the biggest traps people fall into when trying to understand dental insurance is looking only at the monthly premium. A low monthly bill looks great on the surface, but it can be really deceiving if that plan comes with a sky-high deductible or weak coverage, leaving you with massive out-of-pocket bills.

Key Consideration: Think of it like this: a low-premium plan is like a bare-bones car insurance policy with a huge deductible. It’s cheap every month, sure, but if you get in an accident, you're paying a lot more yourself before the insurance company steps in. A plan with a higher premium but a lower deductible gives you more protection right when you need it most.

Your goal is to find that sweet spot where the monthly premium fits your budget, but the out-of-pocket costs for the care you actually expect to need are also manageable.

Where to Find and Compare Plans

Once you have a solid idea of your needs and your budget, it's time to start shopping. For our neighbors in Surprise and Peoria, there are a few common places to look for dental insurance:

- Through Your Employer: This is usually the most affordable route. Employers often pay for a chunk of the premium, and since it’s typically a pre-tax benefit, it also lowers your taxable income.

- The Healthcare Marketplace: If you're self-employed or your job doesn't offer dental benefits, you can find and compare plans on the state or federal health insurance marketplace.

- Directly from Insurance Companies: You can always go straight to the source and buy a plan directly from an insurance provider's website.

- Through a Private Broker: An insurance broker can be a great resource, helping you sift through multiple plans from different companies to find the one that truly fits your unique situation.

As you compare, don't forget that picking the right dentist is just as crucial as picking the right plan. Our guide on how to choose the right dentist can help you figure out what to look for in a dental team you can trust. And of course, the team here at West Bell Dental Care is always happy to help you check if we are in-network with any plan you're looking at.

Getting the Most from Your Dental Benefits

Having a dental insurance plan is a great first step. But to really protect your health and your wallet, you need to know how to use those benefits wisely. It's about more than just carrying the card in your wallet; it’s about making your plan actively work for you all year long.

So, what's the single best way to get the most from your coverage? Use it for what it’s best at: prevention.

Think about it: most plans are designed to heavily favor preventive services, often covering them at or near 100%. This is your insurance company's way of encouraging you to catch small issues before they become big, expensive problems. It's a win-win.

Be Strategic with Your Benefits

Scheduling your regular cleanings and check-ups is easily the smartest financial move you can make with your dental plan. These appointments are your first line of defense, helping you steer clear of more complex and costly procedures down the road. You can learn more about how our approach to preventive dentistry helps you maintain stronger teeth and keep future costs down.

Beyond just showing up for cleanings, managing your benefits effectively comes down to a few key actions:

- Track Your Annual Maximum: Always have a rough idea of how much your plan will pay for your care in a given year. If you know you need significant dental work, we can help you strategically time your treatments to stay within that limit.

- Know Your Deductible: Keep an eye on when you’ve met your annual deductible. Once it’s paid, your insurance starts sharing the costs. This makes it the perfect time to schedule any procedures you've been putting off.

- Use It or Lose It: This one is crucial. Most dental benefits don't roll over. Your annual maximum resets every year, so any funds you haven't used by the deadline are simply gone.

Your Partners in Care: At West Bell Dental Care, we see ourselves as your dedicated partners in this process. Our job isn't just to provide excellent clinical care. We're also here to handle the administrative headaches so you can focus completely on your health.

For our patients here in Surprise, Sun City, and Peoria, your plan is a valuable asset for protecting your smile and your budget. Our staff will help you make the most of it by verifying your coverage, submitting all claims on your behalf, and giving you clear, detailed cost estimates before any work ever begins.

Our goal is simple: to take the financial uncertainty out of your dental care. We always invite you to contact us with any questions about your specific plan. We're here to help.

Frequently Asked Questions

Understanding the fine print of dental insurance can bring up a lot of questions. Here are clear, concise answers to some of the most common things we're asked by our patients in Surprise, AZ.

Do you take my insurance plan at West Bell Dental Care?

We are proud to be an in-network provider for a wide range of major dental insurance plans. Because networks can change, the best way to confirm your coverage is to call our Surprise office directly. Our friendly team will happily verify your benefits and help you understand your out-of-pocket costs.

What if I don’t have any dental insurance?

We believe everyone in our community deserves access to quality dental care, with or without insurance. We offer a fantastic in-house dental membership club that provides discounts on services for a low annual fee. We also work with third-party financing companies to make care affordable for our patients in Surprise and Sun City West.

Why wasn’t my dental procedure 100% covered?

This is a very common question, and it's because most plans are designed for cost-sharing. Outside of preventive care like cleanings, you will almost always have some out-of-pocket responsibility. This is determined by your deductible (what you pay first), your coinsurance (the percentage you pay), and your plan’s annual maximum.

Should I choose a plan with a lower premium or a lower deductible?

This depends on your expected dental needs for the year. If you only anticipate routine check-ups for your family, a lower-premium plan can save you money. However, if you think you might need more extensive work, like a crown or filling, a plan with a lower deductible could save you more money on the actual treatment, even with a higher monthly premium.

Is it better to see an in-network or out-of-network dentist?

Seeing an in-network dentist like West Bell Dental Care is almost always the most cost-effective choice. We have pre-negotiated rates with insurance companies, which means your out-of-pocket costs for services will be significantly lower. While PPO plans allow you to go out-of-network, you will pay a higher portion of the bill yourself.

At West Bell Dental Care, we are committed to making every part of your dental experience, from understanding insurance to receiving treatment, as clear and stress-free as possible. If you live in Surprise, Peoria, or any of our nearby communities, please contact our friendly team to ask questions or schedule your next visit. We look forward to seeing you!